UAD 3.6 and Your Fees: Will You Actually Get Paid More?

Here's the question I hear more than any other right now: "If UAD 3.6 reports take 50% longer, will I get paid 50% more?"

The honest answer is: probably not 50% more. But the fee picture is more interesting - and more favorable - than most appraisers realize. Especially if you're willing to think beyond lender work.

Let me break down the math.

The Production Problem Nobody Wants to Say Out Loud

Let's start with what's actually happening to your time.

A typical full interior appraisal currently takes 5-7 hours from inspection to delivery. Under UAD 3.6, industry estimates put the initial learning curve at 25-50% more time per report. That means a report that takes you 6 hours today might take 7.5-9 hours for the first several months. (Financial impact analysis)

One appraiser blogger laid it out as plainly as anyone: "If reports take longer to complete, one of three things must happen. Appraisers produce fewer reports, fees increase to offset time, or quality compresses under volume pressure." (Kenney Appraisal)

That's the production equation. More time per report means either fewer reports, higher fees, or cutting corners. There's no fourth option.

For a busy appraiser completing 15-20 reports per month, the first few months of UAD 3.6 could mean a noticeable revenue dip — not because you're working less, but because each report takes longer at the same fee.

An appraiser on Reddit put the frustration into sharp focus: "I get near $650 right now on conventional 1004s. If this new form is going to take 1.5 times longer why aren't we raising fees by that much?" (Reddit)

Fair question.

What the Data Actually Says About Fees

Over 40% of appraisers surveyed expect their fees to increase under UAD 3.6. But 28% anticipate fees will stay the same, and 31% aren't sure. (Appraisal Today)

That's a split market. And the split tells you something important: fee increases won't happen automatically. They'll happen for appraisers who proactively adjust their rates and have the positioning to back it up.

Here's why some appraisers will get higher fees and others won't.

The supply side is shifting. Appraisers are retiring. Some are quitting specifically because of UAD 3.6. The workforce has already declined from 98,450 in 2007 to roughly 78,800. Every appraiser who exits the market means slightly more demand for the ones who stay. Fewer appraisers plus steady order volume equals upward pressure on fees. It won't happen overnight, but the trend line favors the appraisers who remain.

Lenders will need UAD 3.6-competent appraisers. In the months surrounding the November deadline, lenders will be looking for appraisers who can reliably deliver compliant UAD 3.6 reports. If you're one of the ones who practiced during the dual-format period and can deliver clean reports without hand-holding, you'll have leverage. If you waited until November and you're still figuring out the interface, you won't.

AMCs will still resist fee increases. This is the reality. AMCs are in the business of compressing fees. UAD 3.6 doesn't change that incentive structure. Some AMCs may adjust their fee schedules to reflect the additional work. Many won't - at least not voluntarily. If you're depending on AMCs to proactively pay you more, you'll probably be disappointed.

The Fee Conversation You Need to Have Now

If you're going to raise your fees - and the production math says you should, at least temporarily - have the conversation before November. Not after.

Here's the logic: during the dual-format period (now through November 1), you can demonstrate UAD 3.6 competency while fees are still being negotiated. Lenders and AMCs who see you delivering clean 3.6 reports will be more receptive to a fee adjustment than ones who hear about it for the first time when they're scrambling to find compliant appraisers in November.

The argument is straightforward. Something like: "The new UAD 3.6 reporting requirements involve significantly more data collection and structured documentation than the previous format. During the initial transition period, I'm adjusting my fee schedule to reflect the additional time. My UAD 3.6 rate for a full interior appraisal is $X."

You don't need to apologize for it. You don't need to explain the entire UAD 3.6 transition. State the rate, state the reason, and let the market decide.

Some appraisers I work with are handling this by quoting UAD 3.6 reports at a separate (higher) rate during the transition period. Others are building the increase into their standard rate now. Either approach works - the key is having the conversation proactively rather than absorbing the extra time at the old fee.

The Math That Changes Everything

Here's where the fee conversation gets really interesting - and where it connects to something bigger than UAD 3.6.

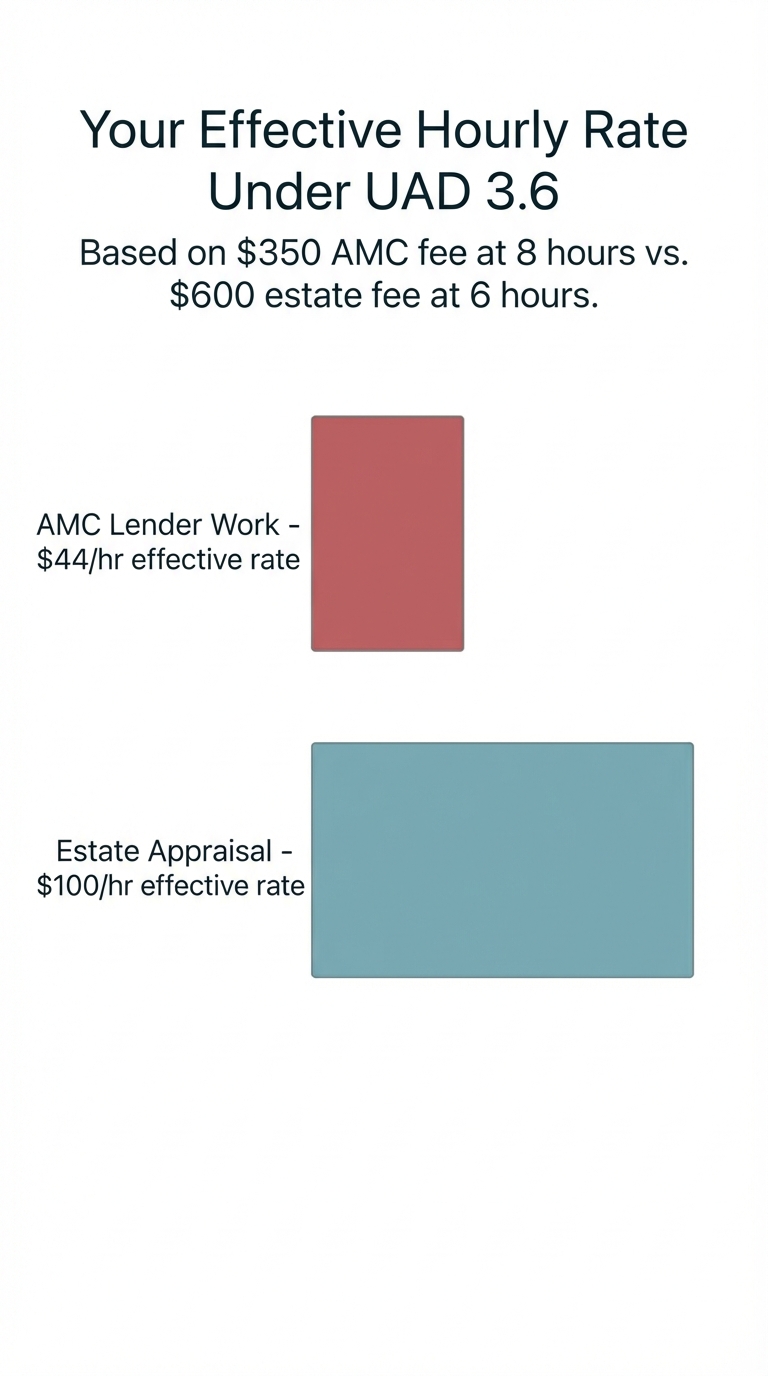

If your average AMC order pays $350 and a UAD 3.6 report takes you 8 hours instead of 6, your effective hourly rate just dropped from about $58/hour to about $44/hour. That's before overhead.

Now compare that to non-lender work:

An estate appraisal at $600 takes roughly the same time as a lender appraisal - but uses a narrative report format, not UAD. No structured data fields. No room-level dropdown entries. No UAD compliance checks. Your effective hourly rate: $100/hour.

A divorce appraisal at $750? Even better.

The UAD 3.6 transition is making an already stark fee disparity even starker. The gap between what AMCs pay and what private clients pay was always significant. Now that lender reports take even longer, the gap widens.

I'm not saying abandon lender work. I'm saying this is the moment to seriously evaluate your client mix. If 80% of your revenue comes from AMC work at $300-400 per report, and those reports just got 25-50% longer, the math is telling you something.

For more on building the non-lender side, see UAD 3.6 Doesn't Apply to Your Most Profitable Work and The Appraiser's Guide to Finding Private Clients.

The Recovery Timeline

The time increase is real, but it's also temporary.

Most appraisers I talk to expect to recover to normal productivity within 3-6 months of regular UAD 3.6 use. The learning curve is steepest in the first few weeks as you learn the new interface and adjust your inspection workflow. By report number 10-15, most of the unfamiliar becomes routine.

That means the fee pressure is heaviest in the first few months after you switch over. If you start now - during the dual-format period - you can absorb the learning curve while UAD 2.6 is still available as a fallback. By the time November arrives, you'll be close to normal speed while the appraisers who waited are just starting their learning curve.

This is one of the strongest arguments for practicing now rather than waiting. The appraisers who are fast and competent on UAD 3.6 in November will command better fees than the ones who are slow and uncertain.

The Bottom Line on Fees

Will UAD 3.6 get you paid more? Here's the honest answer.

Short-term (first 3-6 months): Expect to make less per hour on lender work unless you proactively raise your fees. The additional time is real and it directly impacts your effective rate.

Medium-term (6-12 months): As the workforce contracts and UAD 3.6 becomes mandatory, fee pressure should ease for competent appraisers. Supply and demand will help, but don't expect dramatic increases.

Long-term: The appraisers who come out of this transition in the strongest financial position won't be the ones who negotiated slightly better AMC fees. They'll be the ones who used the transition as motivation to build a more balanced client base - one where non-lender work at $500-$1,000 per assignment makes up a growing share of their revenue.

The fee question isn't really about UAD 3.6. It's about whether you're willing to stop depending on a system that was already underpaying you before the forms changed.

Related Articles:

Jon Barrett

Jon Barrett is the founder of Appraiser Machine and has spent over a decade working with independent appraisers. He's built 300+ appraiser websites, co-led a national appraiser mastermind group, and talked with hundreds of appraisers about what's actually working in their practices. He built Appraiser Machine because the operations side of running an appraisal practice was still stuck in spreadsheets and duct tape - and appraisers deserved better.