What Is UAD 3.6? A Simple Guide for Appraisers

The last time the industry changed forms, half the appraisers I work with said they were going to retire. Most of them didn't. They grumbled for a few months, figured it out, and kept going.

UAD 3.6 is triggering that same conversation - except this time, the changes are actually bigger. The timeline is tighter. And the people saying "I might just be done" sound like they mean it a little more than last time.

I've spent the last decade building tools for appraisers and talking to hundreds of you about what's working and what's broken in your practice. Over the last year, UAD 3.6 has come up in nearly every single conversation. And what I keep hearing is some version of: "I know it's coming. I know I need to deal with it. But I still don't really understand what's actually changing."

So here it is. Plain English. No regulatory jargon. No panic. Just what UAD 3.6 actually is and what it means for your daily work.

The Short Version

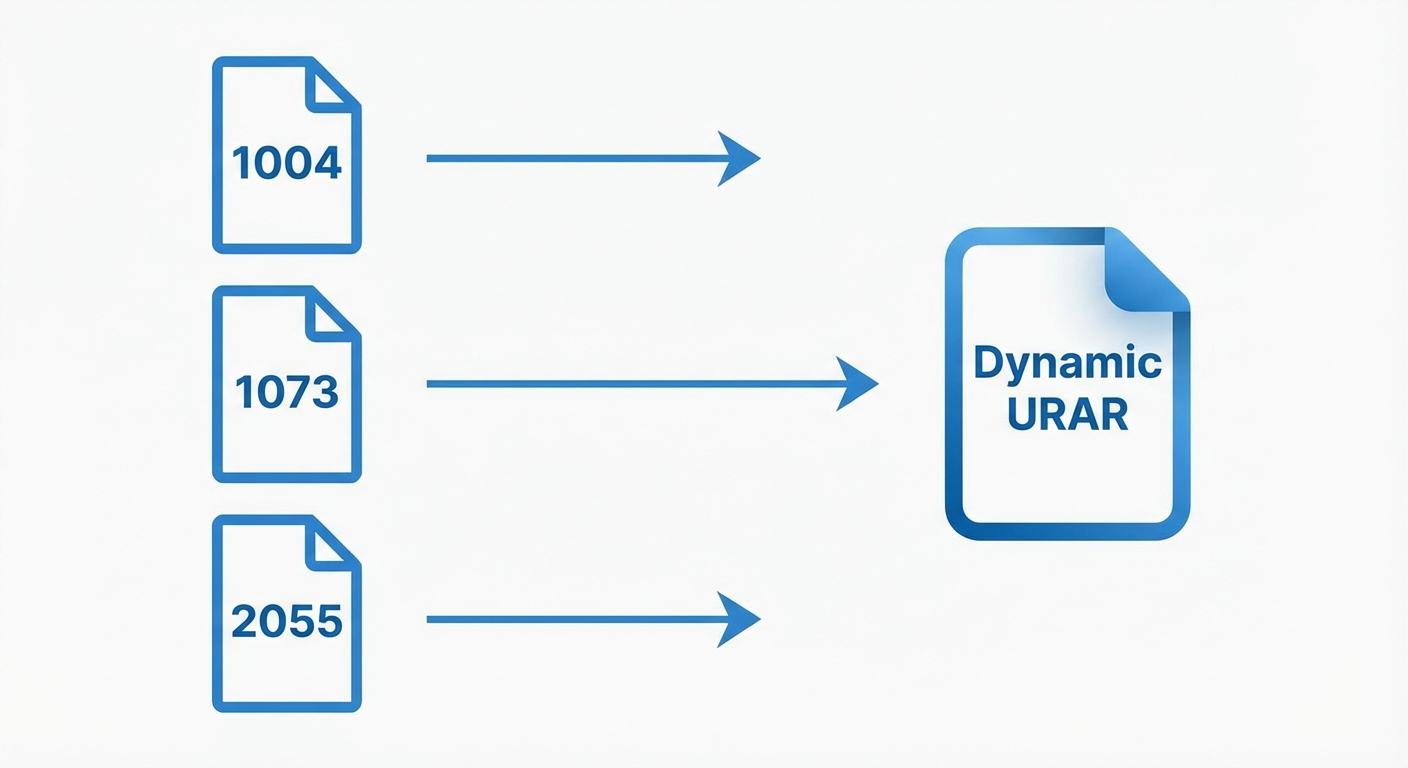

UAD 3.6 is a complete rebuild of the data format that Fannie Mae and Freddie Mac require for residential appraisal reports. It replaces everything you've been using since 2011 - every legacy form, every familiar field layout, every report structure you've memorized over the last 15 years.

The 1004 is retiring. So is the 1073, the 2055, and the rest. All of them get replaced by a single dynamic report called the Uniform Residential Appraisal Report (URAR) that adapts based on the property type, loan type, and scope of work.

That's worth repeating: there is no more choosing between forms. There is one report. It changes shape depending on what you're appraising and how you're appraising it.

As Fannie Mae's own FAQ puts it - the data that describes the subject property now drives the report, not a form number. (Fannie Mae UAD 3.6 FAQ)

If you've been filling out 1004s for 20 years and can do it in your sleep, this is the most disorienting part of the change. Not because the new system is harder. Because the muscle memory stops working.

Why This Is Happening

Understanding the "why" makes the "what" easier to accept.

The GSEs want machine-readable data. That's the whole game. They want every appraisal report to feed into automated risk models, underwriting systems, and compliance databases without a human having to interpret a narrative paragraph or decode inconsistent formatting.

Under the old system, two appraisers could describe the same property condition in completely different ways, and both would be "correct" because there was room for free-form interpretation. Under UAD 3.6, that same condition gets captured as structured data - specific values selected from defined options. Less ambiguity. More consistency. Easier for machines to process.

One appraiser on Reddit called it "the biggest disruption since the computer." That might not be far off. But as another pointed out in the same thread - the revision request log that comes with it "marks a rare advantage for appraisers." The change cuts both ways.

You might have feelings about whether this is a good direction for the profession. I certainly hear plenty of opinions from appraisers on the topic. But the reality is that it's happening, it's mandatory in November, and your opinion about the wisdom of the change doesn't change the deadline.

The Big Changes at a Glance

I want to keep this article at the overview level. For the detailed, practical breakdown of what changes in your daily workflow - the specific fields, the dropdown examples, the narrative shifts - I wrote a full walkthrough in How UAD 3.6 Changes Appraisal Reports. What follows are the headlines.

One dynamic report replaces all legacy forms. No more choosing between the 1004, 1073, 2055, and the rest. You describe the property and the scope of work, and the report adapts. Your software handles the layout logic.

More structured data, less free-form writing. Much of what used to be narrative description is now captured through checkboxes, dropdowns, and defined data fields. Narratives still exist in key sections, but the ratio shifts toward structured data entry.

Room-level detail is now required. Dimensions, condition, and materials for individual rooms. Ceiling height for every room. This is the change that adds the most time to inspections and reports initially.

New sections for energy efficiency and disaster mitigation. Structured fields for HVAC, insulation, solar panels, storm shutters, roof strapping, and more. These sections didn't exist before.

Condition and quality ratings split into interior and exterior. The C1-C6 and Q1-Q6 scale stays, but you rate interior and exterior separately. Quality ratings get plus/minus modifiers. Updated definitions are published and worth reviewing. (C&Q Rating Definitions PDF)

New delivery format. Reports get delivered as a ZIP package containing the XML data file, a human-readable PDF, and all photos/exhibits. Your software builds the package.

Two Things That Actually Got Better

It's not all bad news. Two changes are genuine improvements that appraisers I talk to are actually glad about.

Comp drive-bys are gone. Fannie Mae retired the requirement to physically drive to each comparable sale. You still need comp photos, but how you source them is your call. For anyone covering a large geographic area, this saves real time. (Fannie Mae Appraiser Update)

Revision requests now leave a paper trail. For the first time, there's a built-in log documenting who requested a revision, when, and what they asked for. If you've ever dealt with unreasonable revision pressure from an AMC, that documented trail changes the dynamic.

There's also a new table called "Additional Properties Analyzed But Not Used" where you document comps you considered but didn't include - and why. If you've ever gotten a revision request that amounted to "why didn't you use 123 Main Street?" this table lets you answer that question before it's asked.

The Timeline

We're currently in what Fannie Mae calls "Broad Production." Lenders can request either UAD 2.6 or 3.6 right now. After November 2, 2026, it's UAD 3.6 only for all new GSE submissions.

January 26, 2026 - Broad Production opened. We're here now.

Spring 2026 - FHA systems get updated for optional UAD 3.6 delivery.

November 2, 2026 - Mandatory. All new GSE appraisals must use UAD 3.6.

May 3, 2027 - UAD 2.6 fully retired. No more revisions on legacy reports.

Source: Freddie Mac Official Timeline

That gives you about eight months. Enough time to prepare if you start now. Not enough time if you wait until October.

What UAD 3.6 Does NOT Change

This part matters as much as the changes.

USPAP is the same. Your professional standards, ethics, and independence requirements haven't changed. UAD 3.6 is a data format change, not a standards change.

Your analysis is the same. You're still finding comps, making adjustments, and forming a credible opinion of value. The analytical work is unchanged.

Your professional judgment still drives the report. Nobody is automating your conclusions. You inspect, you analyze, you certify.

And here's the one that deserves its own paragraph: UAD 3.6 does not apply to non-lender work. Estate planning, divorce valuations, tax appeals, pre-listing appraisals - none of it requires UAD formatting. Those assignments are completely unaffected by this transition.

I'll say more about why that matters in UAD 3.6 Doesn't Apply to Your Most Profitable Work. But the short version: if you're looking to reduce the stress of this transition, building a stronger non-lender client base is one of the smartest moves you can make right now.

How Long Will This Take to Learn?

The honest answer: it depends on how quickly you start practicing.

Industry estimates suggest reports will take 25-50% longer during the initial learning curve. That's real, and it affects your fee math. But the first appraiser to successfully submit a UAD 3.6 report described the process as "far easier than anticipated." (SFREP)

Most appraisers I talk to expect to recover to normal productivity within 3-6 months. The learning curve is real. It's also temporary.

The appraisers who will have the hardest time are the ones who don't touch UAD 3.6 until November 1. The ones who start now - even with a single mock report - will have the smoothest transition.

Where to Start

If this article is your first real look at UAD 3.6, here's what I'd do next.

Read the UAD 3.6 Checklist for Appraisers. It's the step-by-step preparation plan with specific training resources, software guidance, and inspection workflow changes.

If you want to understand the daily workflow impact in detail - the specific fields, the dropdown examples, how narrative writing changes - see How UAD 3.6 Changes Appraisal Reports.

And for the side-by-side comparison you can bookmark and reference during the transition, UAD 3.6 vs Current UAD is the reference piece with all the tables and official resource links.

The deadline isn't moving. But eight months is more than enough time to be ready - if you use them.

Related Articles:

Jon Barrett

Jon Barrett is the founder of Appraiser Machine and has spent over a decade working with independent appraisers. He's built 300+ appraiser websites, co-led a national appraiser mastermind group, and talked with hundreds of appraisers about what's actually working in their practices. He built Appraiser Machine because the operations side of running an appraisal practice was still stuck in spreadsheets and duct tape - and appraisers deserved better.