The UAD 3.6 Liability Question Nobody's Talking About

There's a question circulating in appraisal forums that most UAD 3.6 training courses skip over entirely: does more data mean more liability?

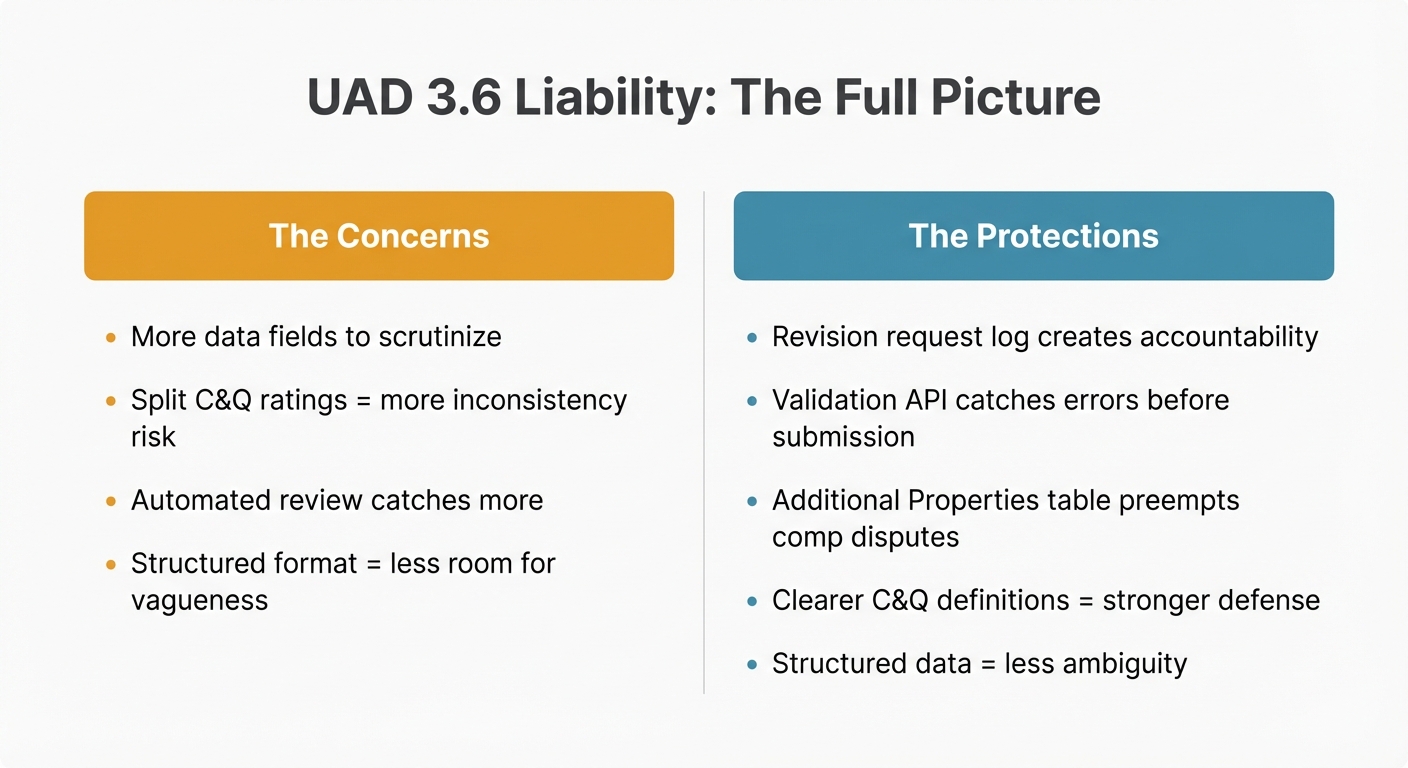

It's not a paranoid question. It's a practical one. Under UAD 3.6, you're documenting more fields, providing more structured data, and creating a more detailed record of your analysis than ever before. Condition and quality ratings are split into interior and exterior. Room-level detail is required for every room. Energy efficiency, disaster mitigation, and comp rejection reasoning all get documented in structured fields.

More data points mean more places where someone can disagree with you. More fields mean more potential errors. More structured documentation means a more detailed paper trail.

On AppraisersForum, appraisers have been raising this concern directly - expanded commentary expectations leading to more revision requests and elevated E&O exposure. (AppraisersForum discussion)

The anxiety is understandable. But the full picture is more nuanced - and in some ways, more favorable - than the fear suggests.

The Liability Concern, Stated Plainly

Here's the worry, stripped of jargon.

Under the old system, you wrote a narrative. "Property is in average condition. Kitchen was updated approximately 5 years ago. Roof appears to be in typical condition for age." There was room for interpretation. The narrative was yours. The judgment was yours. And if a reviewer disagreed, the dispute was about a paragraph of text.

Under UAD 3.6, you're selecting from defined values. Interior condition: C3. Exterior condition: C4. Kitchen flooring material: Ceramic Tile. Roof condition: Fair. Each of these is a discrete data point that can be individually validated, compared against photos, and flagged by automated systems.

The concern is that structured data makes it easier for lenders, AMCs, and regulators to find things to question. Instead of debating the tone of a narrative, they can point to a specific field and say "this value doesn't match our expectations."

That's a legitimate concern. And I won't pretend it's baseless.

But Here's What Most Appraisers Are Missing

The same structured data system that creates more scrutiny also creates more protection. And in some important ways, UAD 3.6 actually tilts the playing field toward the appraiser for the first time in years.

The revision request log. This is the biggest change most appraisers aren't paying attention to.

For the first time in the history of the profession, revision requests are formally documented. Who requested the revision. When they requested it. What they asked for. Every request leaves a trail.

As one appraiser on Reddit noted, this "marks a rare advantage for appraisers."

Think about what that means in practice. Under the current system, an AMC reviewer can call and pressure you to change your value conclusion, and there's no record of the conversation. They can email you a vague "please reconsider" request, and if you push back, it's your word against theirs.

Under UAD 3.6, that interaction is logged. If a lender asks you to change a condition rating from C4 to C3 without providing compelling evidence, that request is documented. If an AMC pressures you to adjust your value, the pressure is visible.

For appraisers who have dealt with years of unreasonable revision requests - and I hear about this constantly from the appraisers I work with - the documented log is genuinely protective. It creates accountability that didn't exist before.

The "Additional Properties" Table Preempts the Most Common Dispute

One of the most frequent revision triggers under the current system is comp selection. "Why didn't you use the sale at 123 Main Street?" "We think comparable #3 should have been replaced with this property."

Under UAD 3.6, the new "Additional Properties Analyzed But Not Used" table gives you a formal place to document the comps you considered and rejected, with your reasoning. (Enact MI)

This is preemptive defense. Instead of waiting for the reviewer to question your comp selection and then explaining after the fact, you document your reasoning up front. "I considered 123 Main Street but excluded it because the sale conditions were atypical (REO with below-market pricing)."

That doesn't eliminate comp selection disputes entirely. But it addresses the most common one before it starts. Over time, this should meaningfully reduce revision cycles.

Structured Data Cuts Both Ways (But Favors Careful Appraisers)

Here's a counterintuitive point: more structured data may actually reduce certain types of liability exposure.

Under the old narrative system, ambiguity was everywhere. What does "average condition" mean? What does "typical for the area" mean? These phrases are subjective, and subjectivity invites disagreement.

Under UAD 3.6, when you rate a kitchen's condition as C3 and select specific material types from defined dropdowns, there's less room for misinterpretation. It's easier to question a specific data point, but it's also easier to defend one. "I rated the interior condition C3 because the kitchen was updated 5 years ago with standard-quality materials and shows normal wear consistent with the C3 definition" is a more defensible position than "I described the condition as average."

The updated C&Q definitions provide clearer guidance for each level, which gives you stronger ground to stand on when ratings are challenged. (C&Q Rating Definitions PDF)

The Pre-Submission Validation API Catches Errors Before They Become Problems

Under the current system, you submit a report and hope it doesn't come back with issues. Under UAD 3.6, software can run compliance checks against UAD rules before the report is submitted to UCDP. (ValueLink)

This is the quality control step that catches missing fields, data inconsistencies, and formatting errors before they reach the lender. It's not a guarantee against revision requests, but it eliminates the category of "you forgot to fill in this field" rejections that waste everyone's time.

Think of it as a spell-check for compliance. It doesn't judge your analysis. It checks whether all required fields are populated and whether the data is internally consistent.

What the E&O Picture Actually Looks Like

So does UAD 3.6 increase your E&O exposure?

The honest answer is: it shifts it. Some risks decrease. Some risks are new.

Decreased risk: Ambiguity-based disputes become harder when data is structured and specific. The revision request log creates accountability for unreasonable pressure. The validation API catches submission errors before they become defects. The "Additional Properties" table preempts comp selection challenges.

New risk: More data fields mean more individual points that can be scrutinized. Split interior/exterior C&Q ratings mean inconsistencies between your ratings and your narrative are more visible. The structured format makes automated review easier - which means lender QC systems will flag more reports for review.

Net effect: For appraisers who are thorough and consistent in their documentation, the net effect is likely positive. The tools that come with UAD 3.6 - the revision log, the validation checks, the comp rejection documentation - provide protections that didn't exist before.

For appraisers who are sloppy with their documentation, the net effect is negative. Structured data makes inconsistencies more visible, not less. If your interior condition narrative contradicts your C/Q rating, that contradiction is now easier to catch.

The takeaway: UAD 3.6 rewards careful, consistent documentation and penalizes careless documentation. If you're already thorough in your work, the new system is actually more protective than the old one.

Practical Steps to Manage Liability Under UAD 3.6

Review the updated C&Q definitions before your first report. The split between interior and exterior ratings is the most likely source of inconsistencies. Know the definitions cold. (Download them here.)

Use the "Additional Properties" table on every report. Don't leave it blank. Document at least 2-3 comps you considered and rejected. This is your preemptive defense against the most common revision request.

Run the validation check before every submission. Make it part of your workflow. Catch the easy errors before they reach UCDP.

Keep your narratives consistent with your structured data. If you rate a kitchen C3, your narrative should support that rating. If you describe recent upgrades, the condition rating should reflect them. Consistency between structured data and narrative is the single biggest factor in avoiding disputes.

Document your reasoning, not just your conclusions. The structured format captures what you observed. Your narratives should capture why you made the judgments you did. "I rated the exterior C4 because while the roof was replaced 3 years ago, the siding shows deferred maintenance consistent with..." That kind of reasoning is defensible.

For a systematic approach to catching these issues before submission, see how Revision Shield works inside Appraiser Machine - a 143-item residential (and 65-item commercial) Pre-Submit QC checklist with AI Contradiction Detection that reads the whole report at once and flags cross-section inconsistencies. It was built specifically to catch the kind of issues that trigger revision requests.

The Bottom Line on Liability

UAD 3.6 doesn't increase your liability. It increases your visibility.

If your work is thorough, consistent, and well-documented, that visibility works in your favor. The revision log protects you. The structured data supports you. The validation checks catch your mistakes before anyone else sees them.

If your work is inconsistent or careless, that visibility works against you. Automated review systems will flag more discrepancies, and the structured format makes those discrepancies harder to explain away.

The appraisers who take the time to learn the new C&Q definitions, use the "Additional Properties" table, and keep their narratives consistent with their structured data will find that UAD 3.6 is actually a more protective system than the one it replaces.

The ones who don't will have a harder time than before.

That's not a threat. It's an incentive to be the thorough professional you already are.

Related Articles:

Jon Barrett

Jon Barrett is the founder of Appraiser Machine and has spent over a decade working with independent appraisers. He's built 300+ appraiser websites, co-led a national appraiser mastermind group, and talked with hundreds of appraisers about what's actually working in their practices. He built Appraiser Machine because the operations side of running an appraisal practice was still stuck in spreadsheets and duct tape - and appraisers deserved better.