How to Price Private Appraisals: A Fee Guide for Non-Lender Work

Here's a conversation that happens more often than it should.

An estate attorney calls. They need a date-of-death valuation for a probate case. The property is a standard 3-bed/2-bath in a suburban neighborhood. The appraiser quotes $375.

Why $375? Because that's what the AMCs pay. It's the number that's been burned into the appraiser's brain as "what an appraisal costs."

The attorney would have paid $650 without blinking. The estate covers the cost. The amount is insignificant relative to the legal fees already involved. But the appraiser never found out because they quoted their AMC rate reflexively.

I've seen this happen hundreds of times across the appraisers I work with. The skills transfer perfectly from lender to non-lender work. The pricing psychology doesn't. And it's costing you real money.

Why AMC Pricing Doesn't Apply to Private Work

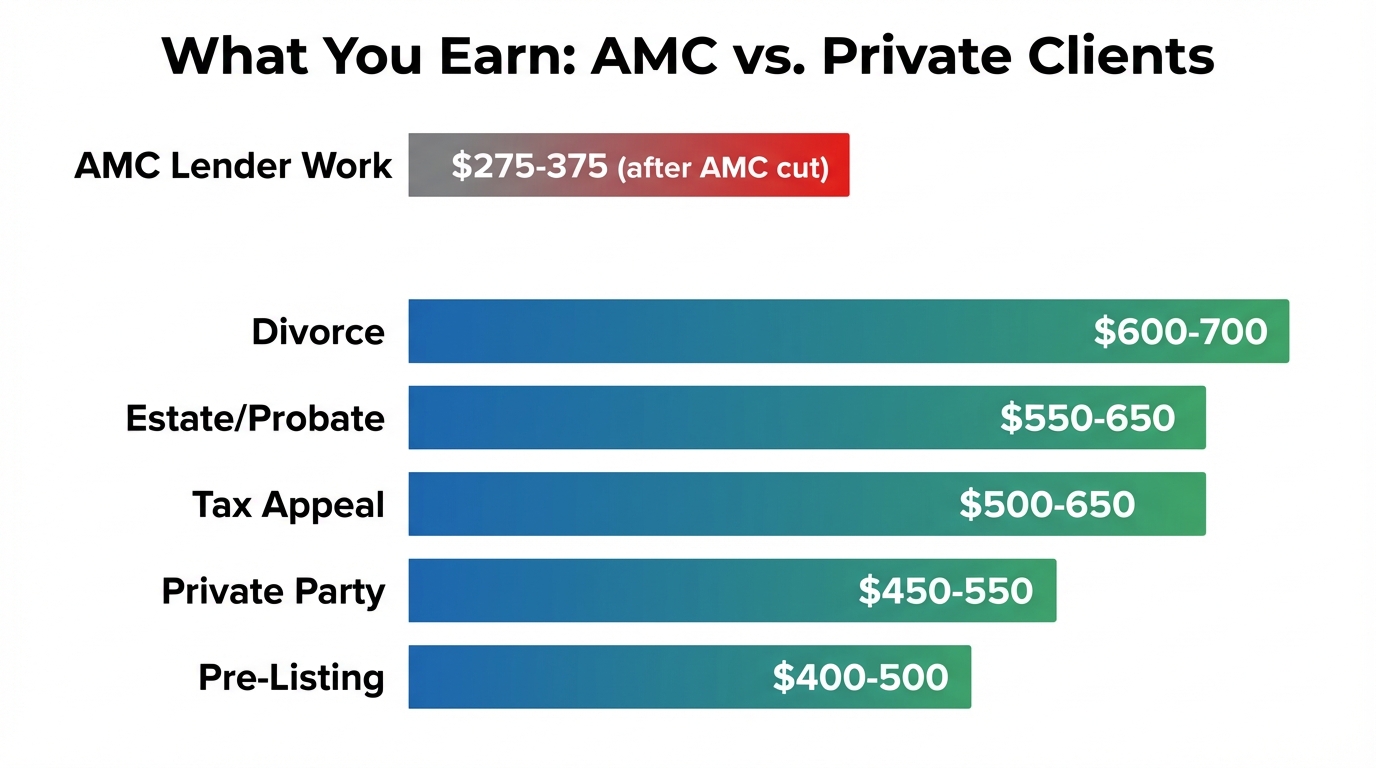

AMC fees are not market rates. They're compressed rates that exist because AMCs operate as intermediaries who take 30-50% of the total fee before passing the remainder to you. A $550 appraisal order from a lender becomes a $300 payment to you after the AMC's cut.

When you do private work, there is no AMC. You're being hired directly by the attorney, the homeowner, or the CPA. The full fee goes to you. Your pricing should reflect the direct service model, not the intermediary model.

Non-lender clients expect to pay more because they're getting more: direct communication with the appraiser, customized reporting for their specific use, faster turnaround since there's no AMC review layer, and your full attention on their assignment.

As one appraiser on AppraisersForum put it - you wouldn't use C5/Q4 UAD ratings on a divorce appraisal. The work is different. The pricing should be too.

The Fee Framework

After working with hundreds of appraisers on their non-lender pricing, here's the framework I recommend. These ranges reflect what I've seen across appraisers in various markets — your local rates may differ based on geography, competition, and property complexity.

| Service Type | Standard Fee | Premium Fee | Rush Add-On |

|---|---|---|---|

| Estate/Probate | $550-650 | $750+ | +25-50% |

| Divorce | $600-700 | $800-1,000 | +25-50% |

| Tax Appeal | $500-650 | $750+ | +25-50% |

| Pre-Listing | $400-500 | $600+ | +25% |

| Private Party | $450-550 | $650+ | +25% |

| Expert Witness | $600-800 base | $1,200+ | Hourly testimony |

Premium pricing applies to complex, large, or high-value properties. An estate valuation on a $2 million waterfront property warrants a higher fee than a $200,000 ranch. Adjust accordingly.

Rush pricing applies when the client needs the report faster than your standard turnaround. Attorneys often have court deadlines. A 25-50% rush fee is standard and expected.

How to Communicate the Fee (Without Apologizing)

This is where most appraisers struggle. Not because the fee is unreasonable, but because years of AMC conditioning have trained them to negotiate down before the conversation even starts.

Here's the script that works:

"My standard fee for a [type] appraisal is $[X]. That includes a comprehensive inspection, detailed market analysis, and a [court-ready/professional] report delivered within [5-7] business days. Rush service is available for an additional fee. Would you like me to schedule the inspection?"

State the fee. Describe what's included. Ask for the next step. That's it.

What you never say:

- "My fee is usually... but I could do it for..."

- "What were you expecting to pay?"

- "I can match what other appraisers charge."

- "Is that within your budget?"

These phrases signal that your price is negotiable. For most non-lender clients, it isn't. The attorney has a probate case worth $500,000. Your $650 fee is a rounding error in the context of their legal bills. They're not shopping for the cheapest appraiser. They're looking for someone reliable who can deliver a defensible report on time.

The Three Factors That Justify Premium Fees

When you're quoting above-AMC rates, it helps to understand why the market supports these prices. Not as a justification script - but as confidence that your pricing is reasonable.

Direct service. No AMC portal. No 800-number between the client and the appraiser. The attorney or homeowner talks to you directly, gets answers from the person who inspected the property, and has a real professional relationship. That's worth money.

Customized reporting. Non-lender reports are tailored to the specific use case. An estate appraisal includes retrospective analysis. A divorce report includes court-ready documentation. A tax appeal report addresses the assessment specifically. This isn't one-size-fits-all. The work is scoped to the assignment.

Accountability. When an estate attorney hires you, your name is on the report. Not an AMC's name. Not a portal. You. That direct accountability means the client gets a higher standard of care - and they know it.

When Someone Does Push Back on Price

It happens. Not often with attorneys (they're accustomed to professional fees), but occasionally with homeowners ordering private appraisals.

The most common pushback: "I saw appraisals for $300 online." That's an AMC rate for a lender appraisal - a different product for a different purpose. Your response:

"A lender appraisal through an AMC is typically $300-400 because the AMC takes a portion of the fee and the report is formatted for mortgage underwriting. A [type of appraisal] is a direct engagement with full reporting tailored to [the specific purpose]. The fee reflects the direct service and the customized analysis."

Calm. Professional. Factual. No defensiveness. If the client decides the fee is too high, that's their choice. You don't lower your rate to match a product that isn't comparable.

In practice, most non-lender clients don't negotiate. Attorneys expect professional fees. Estate executors are spending estate funds, not personal money. Divorce clients have legal counsel advising them to get a proper appraisal. The rare pushback usually comes from homeowners who don't understand the difference between a lender appraisal and a private one.

Setting Up Your Fee Schedule

A clear, written fee schedule does two things: it makes quoting easier for you, and it makes the fee feel established rather than made up on the spot.

Your fee schedule should list each service type with a base fee, note that complex or high-value properties may be quoted individually, include your rush fee structure, and state your standard turnaround time.

Keep it on your website. Send it to attorneys when they inquire. Include it in your introduction letters. The more established your pricing looks, the less likely anyone is to question it.

One of the features appraisers use most in Appraiser Machine is the Instant Quote Form - a branded form you embed on your website where clients select the appraisal type, see your pricing, and pay to book online. You wake up to a paid order instead of a voicemail you have to return between inspections.

Raising Your Fees Over Time

If you're currently doing non-lender work at AMC rates, don't jump to $650 overnight. A sudden doubling of your fee to existing clients creates friction.

Instead, raise incrementally. $50-75 per quarter. New clients get the current rate. Existing clients get advance notice of the increase. Within a year, you're at market-appropriate pricing without disrupting relationships.

For new non-lender clients you haven't worked with before, quote the full market rate from day one. There's no existing relationship to protect. Start strong.

The Bottom Line on Pricing

Your expertise is the same whether you're filling out a UAD 3.6 report for an AMC or writing a narrative report for an estate attorney. The difference is who you're working for and how the transaction is structured.

Non-lender clients pay more because they're paying you directly, because the work is customized, and because they value direct professional relationships. Your pricing should reflect that reality - not the compressed rate an AMC decided your time was worth.

For the full guide to finding these clients, see The Appraiser's Guide to Finding Private Clients Who Pay 2x What AMCs Do. For all seven types of non-lender work and their fee ranges, see 7 Types of Non-Lender Appraisal Work.

Related Articles:

Jon Barrett

Jon Barrett is the founder of Appraiser Machine and has spent over a decade working with independent appraisers. He's built 300+ appraiser websites, co-led a national appraiser mastermind group, and talked with hundreds of appraisers about what's actually working in their practices. He built Appraiser Machine because the operations side of running an appraisal practice was still stuck in spreadsheets and duct tape - and appraisers deserved better.